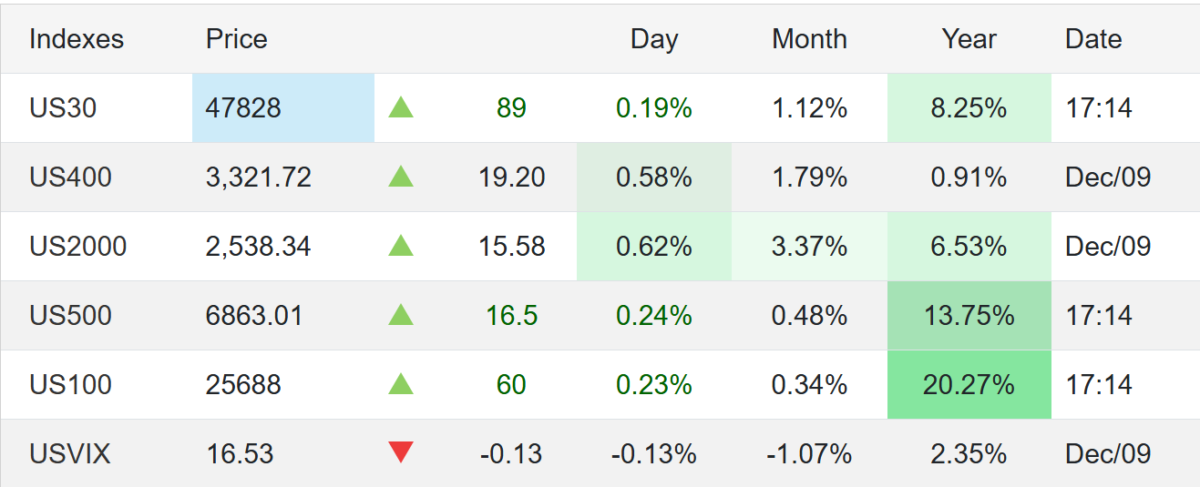

US equities were mostly flat as traders awaited the Federal Reserve’s interest-rate decision.

S&P 500: +0.1%

Dow Jones: +90 points

Nasdaq: Near unchanged

Expectations: Markets are widely pricing in a 25 bp rate cut on Wednesday. Focus is shifting to the Fed’s updated economic projections, especially regarding the pace of policy easing in 2026.

Labor Market

JOLTS (Sept & Oct): Job openings came in above expectations, signaling still-firm demand for labor.

ADP employment (weekly average through Nov 22):

Private employers added ~4,750 jobs per week, ending three straight periods of declines.

US stocks saw limited movements on Monday, with major indexes holding near their record highs from last week. The S&P 500, Nasdaq 100, and Dow Jones Industrial Average all traded flat as investors awaited fresh catalysts, particularly from:

The Federal Reserve’s FOMC meeting minutes

The Jackson Hole Symposium later this week

Both are expected to offer hints on the Fed’s interest rate outlook.

Trade these data points with Swap Hunter by your side and you are going to have an edge on your Broker, your Bank and your Colleagues.

Equities remain supported by growing bets on multiple rate cuts this year, as markets respond to signs of a softening labor market and disinflation pressures.

Key Market Highlights:

Chipmakers and AI-exposed stocks climbed, with Nvidia (+0.5%) staying near record highs despite recent US export controls.

Retail stocks were mixed ahead of upcoming quarterly earnings reports.

Geopolitical backdrop: EU leaders prepared to meet Ukraine’s President Zelensky following US President Trump’s summit with Russian President Putin.

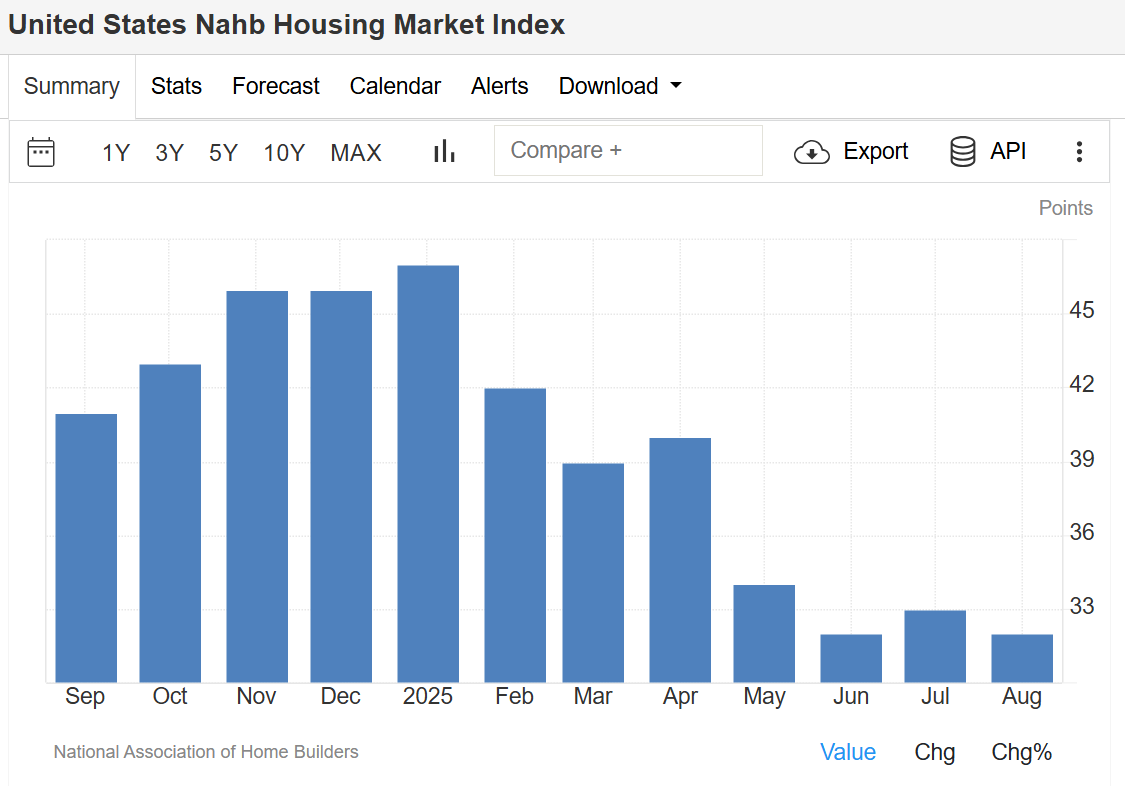

NAHB Housing Market Index – August 2025

The NAHB/Wells Fargo Housing Market Index (HMI) slipped to 32 in August 2025, down from 33 in July and below expectations of 34, signaling persistent challenges in the housing sector.

Breakdown of Housing Data:

Current sales conditions: fell one point to 35

Sales expectations (next 6 months): steady at 43

Buyer traffic: rose two points to 22, still at historically low levels

Builder Incentives & Pricing Trends:

37% of builders cut prices in August (down from 38% in July)

Average price reduction remained at 5% for the tenth straight month

66% of builders used sales incentives, the highest post-Covid level, up from 62% in July

This data reflects ongoing affordability concerns, limited buyer demand, and sustained reliance on incentives to stimulate sales. source: National Association of Home Builders

Stock Market: Investors remain cautious but optimistic, balancing AI-driven growth and monetary policy expectations.

Housing Market: Persistent weakness in builder confidence highlights the impact of affordability challenges, even as incentives expand.

📊 Both markets remain heavily influenced by Federal Reserve policy signals, making this week’s Jackson Hole Symposium a pivotal event for investors and analysts.

Frequently Asked Questions (FAQ)

1. What is the current United States Stock Market Index level in August 2025?

In August 2025, the S&P 500, Nasdaq 100, and Dow Jones remain near record highs after a strong rally earlier in the month. Markets are currently trading flat as investors await signals from the Federal Reserve’s policy outlook.

2. Why are US stocks trading flat despite strong AI and chipmaker performance?

While AI-related stocks like Nvidia continue to perform strongly, overall market movement is subdued due to uncertainty over the Federal Reserve’s interest rate decisions. Investors are waiting for clarity from the Jackson Hole Symposium and FOMC meeting minutes.

3. What does the NAHB Housing Market Index measure?

The NAHB/Wells Fargo Housing Market Index (HMI) measures builder confidence in the housing market, covering current sales, buyer traffic, and future sales expectations. A reading above 50 indicates optimism, while below 50 reflects weakness.

4. Why did the NAHB Housing Market Index fall in August 2025?

The index fell to 32 in August 2025 due to weak buyer demand, affordability challenges, and higher reliance on sales incentives and price cuts by builders.

5. Are US home builders offering more incentives in 2025?

Yes. In August 2025, 66% of builders reported using sales incentives, the highest since the post-Covid period. Price cuts remain common, with an average reduction of 5% per home.

Technical Analysis: S&P 500 – August 2025

The S&P 500 continues to hover near record highs after its sharp rally this summer. Momentum remains strong, but the index is showing signs of consolidation as traders await policy signals from the Federal Reserve.

Key Technical Levels

Resistance Zone: 5,650 – 5,700 → The index is struggling to break above this level, marking a potential short-term ceiling.

Support Levels:

5,500 (near-term support) – A break below could invite short-term selling.

5,350 (major support) – A key level to watch, aligning with the 50-day moving average (50-DMA).

Moving Averages

50-Day Moving Average (50-DMA): ~5,350 – Currently acting as strong dynamic support.

200-Day Moving Average (200-DMA): ~4,950 – Well below current levels, confirming a longer-term bullish trend.

Momentum Indicators

RSI (Relative Strength Index): Hovering around 64, just below the overbought threshold (70). This suggests the index is consolidating but not yet in danger of a deep correction.

MACD (Moving Average Convergence Divergence): Still in positive territory, though momentum is flattening, pointing to a possible range-bound movement in the short term.

Chart Outlook

The S&P 500 remains bullish in the medium to long term, supported by AI-driven growth and easing inflation expectations. However, short-term consolidation is likely until traders get more clarity from Fed policy announcements.

Trading Strategy (Not Financial Advice):

Bullish bias above 5,500 support

Watch for a breakout above 5,700 for continuation toward new record highs

Caution: A sustained break below 5,350 could trigger deeper pullbacks

Former President Donald Trump took aim at Goldman Sachs CEO David Solomon on Tuesday, poking fun at his side gig as a DJ while blasting the bank’s past economic forecasts.

“David Solomon and Goldman Sachs refuse to give credit where credit is due,” Trump wrote on Truth Social. “They made a bad prediction a long time ago on both the Market repercussion and the Tariffs themselves, and they were wrong, just like they are wrong about so much else.”

Inflation Numbers Trigger Trump’s Remarks

Trump’s comments followed the release of the July Consumer Price Index (CPI) report — a key measure of inflation. The Bureau of Labor Statistics reported year-over-year inflation at 2.7%, slightly below analyst forecasts of 2.8%.

The Federal Reserve, led by Chair Jerome Powell, has maintained interest rates while evaluating the inflationary impact of tariffs.

Trump took the latest CPI data as validation of his economic stance:

“It has been proven, that even at this late stage, Tariffs have not caused Inflation, or any other problems for America, other than massive amounts of CASH pouring into our Treasury’s coffers,” he said.

Solomon Joins Growing List of CEO Targets

Solomon is the latest high-profile executive in Trump’s firing line. Just last week, the former president called for Intel CEO Lip-Bu Tan’s resignation — before reversing course after meeting with him at the White House on Monday.

With this latest jab, Trump continues his pattern of publicly challenging corporate leaders, often blending policy criticism with personal ridicule.

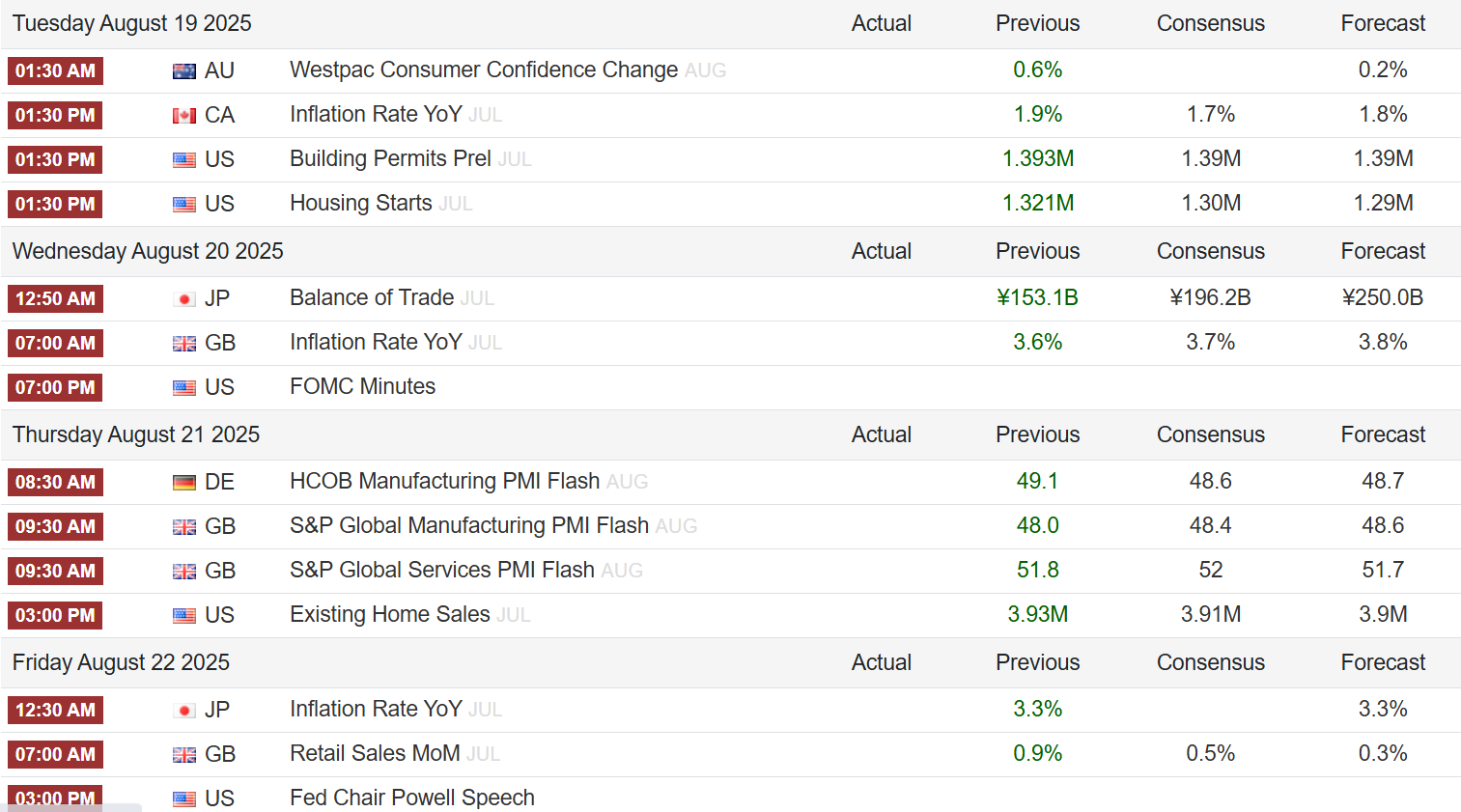

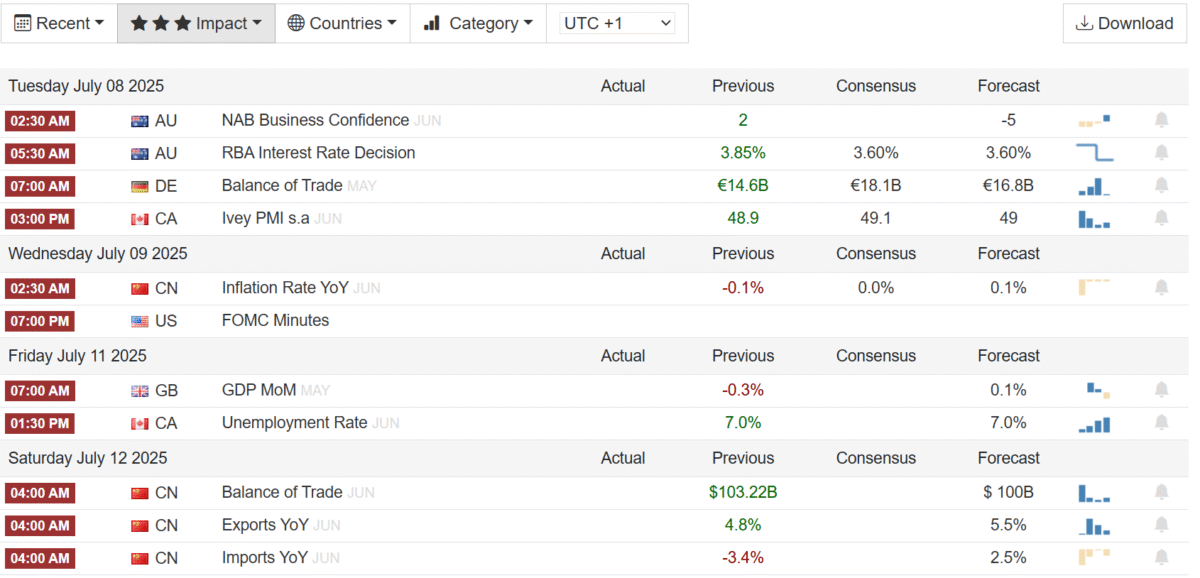

Trade Tensions Return: The July 9th deadline marks the end of the US tariff pause. Only partial deals (UK, Vietnam, China framework) are in place. Markets are bracing for possible escalations and their impact on global trade flows.

Fed Watch: Investors await the FOMC minutes and several Fed speeches to gauge the outlook for interest rates. Chair Powell maintains a cautious tone, but markets want more clues on the path for policy in H2.

Central Bank Decisions: Policy meetings in Australia, South Korea, Malaysia, and New Zealand could signal regional divergence amid slowing global growth and easing inflation.

🇺🇸 United States

Tariff Deadline: High stakes around the July 9th expiration of tariff relief. Key sectors may face higher import costs unless further agreements are reached.

Fed & Data:

FOMC minutes and Fed speeches in focus.

Data includes: Weekly jobless claims, consumer credit, NFIB Small Business Index, and budget statement.

Earnings Season Kickoff:

Watch Delta Air Lines and Conagra Brands earnings on Thursday for early corporate sentiment.

🇨🇦 Canada

June Jobs Report and Ivey PMI will shape expectations around Bank of Canada’s next move.

🇲🇽 Mexico & 🇧🇷 Brazil

Mexico: June inflation report will guide Banxico’s next rate decision.

Brazil: Updates on inflation, retail sales, and business confidence are due.

🇪🇺 Europe

Germany: Expected second monthly industrial production decline, plus trade, wholesale prices, and final inflation data.

Eurozone: First dip in retail sales in 5 months.

UK: Key data on monthly GDP, industrial output, trade balance, and Halifax house prices.

Italy & France: Final inflation and industrial figures.

Others: Switzerland (consumer confidence), Turkey (IP), Russia (inflation).

🌏 Asia-Pacific

China:

CPI likely flat; PPI deflation to ease (still -3.2% y/y).

Japan:

Full slate of data: wages, current account, machine orders, producer prices.

📈 US Stocks Surge as Fed Cut Hopes and Trade Truce Drive Gains

Published: June 30, 2025 Category: Markets & Economy

US equities rallied on Monday, extending last week’s gains as easing trade tensions and growing expectations of interest rate cuts by the Federal Reserve pushed major indexes to record highs.

🔼 Major Indexes Reach New Highs

S&P 500 and Nasdaq 100: Up 0.5% each

Dow Jones Industrial Average: Gained over 200 points

📰 Market Drivers

1. 🇺🇸 US-China Trade Agreement

The US and China announced a formal agreement to prevent new tariffs, with President Trump showing flexibility on the July 9 deadline for reintroducing reciprocal tariffs. This marks a major de-escalation from past tensions, when tariffs reached up to 145%.

2. 🏦 Fed Rate Cut Expectations Rise

Investor confidence is rising as soft inflation data and global uncertainties increase the likelihood of multiple Fed rate cuts in 2025.

3. 💻 Tech Sector Strengthens

Canada scrapped its digital services tax, boosting US tech stocks and reopening trade talks.

Meta and Alphabet shares rose 1%.

Juniper Networks soared 9% after the DoJ approved its HP acquisition, settling a legal dispute.

💶 Eurozone: Euro Hits $1.17 as German Inflation Falls

The euro rose to its highest level since September 2021, trading just above $1.17, bolstered by:

Weaker US dollar from dovish Fed sentiment

Fiscal concerns in the US

Cooling inflation in Germany

🇩🇪 Germany Inflation Back to Target

According to the Federal Statistical Office:

CPI fell to 2.0% in June, down from 2.1%, beating forecasts

Core inflation eased to 2.7%, a 3-month low

Food inflation slowed to 2.0%, energy prices dropped -3.5%

Monthly CPI was flat, following a 0.1% rise in May

🏦 ECB Policy Outlook

While inflation edged up slightly in France, Italy, and Spain, the ECB maintains a cautious approach. Vice President Luis de Guindos reaffirmed that the current policy is appropriate, but warned of the need for flexibility amid economic uncertainty.

Markets continue to price the ECB’s terminal rate around 1.75%–1.80%.

📊 Key Takeaways

✅ US markets are responding positively to reduced geopolitical risk and a potential easing cycle from the Fed.

✅ Eurozone inflation data provides mixed signals but supports a stable ECB outlook.

✅ Tech stocks may continue to benefit from regulatory relief and favorable trade shifts.

European Stocks Climb as Ceasefire Holds, Fed Dovish Tone Lifts Sentiment

Markets held onto their upward momentum Wednesday, with the STOXX 50 and STOXX 600 indices both rising 0.3%, extending gains of over 1% from the previous session. Investors were buoyed by easing geopolitical tensions and growing hopes for a Federal Reserve rate cut later this year.

🌍 Geopolitical Calm Brings Relief

The recent ceasefire between Israel and Iran appears to be holding, providing a much-needed breather for global markets. The truce—brokered by the United States—has helped temper fears of a broader conflict in the Middle East, a key concern for global investors in recent weeks.

📉 Fed Signals Potential Rate Cuts

Further optimism was driven by Federal Reserve Chair Jerome Powell, who gave testimony before the U.S. Congress on Tuesday. His remarks were widely interpreted as dovish, increasing expectations that the Fed could cut interest rates later this year, providing additional support to financial markets.

🔍 Focus Shifts to NATO Summit

Investors are now watching the NATO summit in the Netherlands, where discussions around defense spending and geopolitical stability are taking center stage. Any shifts in policy or alliances could have broader market implications.

Winners on the European Stock Front

Several major companies posted strong gains amid the upbeat mood:

Ferrari (RACE): +3.6%

Stellantis (STLA): +3.7%

ASML Holding (ASML): +2.3%

Philips (PHG): +2.0%

Rheinmetall (RHM): +1.5%

These moves reflect renewed investor confidence across a range of sectors, from luxury autos to defense and technology.

Crude Oil Bounces Back After Heavy Selloff

WTI crude oil prices rebounded above $65 per barrel on Wednesday, recovering some ground after a 13% plunge over the prior two sessions—the steepest two-day fall since 2022.

🔥 What’s Driving Oil?

The ceasefire in the Middle East is reducing supply disruption fears.

President Trump signaled support for China—Iran’s top buyer—to continue importing Iranian oil, potentially reshaping the U.S. sanctions landscape.

Despite this, a preliminary U.S. intelligence report warned that American strikes on Iranian nuclear facilities only delayed the program by a few months, keeping geopolitical risk on the table.

📉 Supply Tightens

Fresh industry data revealed a 4.28 million barrel drop in U.S. crude inventories last week, smashing forecasts for just a 0.6 million barrel draw. This marks the fourth consecutive weekly decline and signals tightening supply conditions.

🧠 Final Thoughts

Markets are finding their footing amid complex global dynamics. While the ceasefire and dovish Fed tone provide near-term relief, investors remain cautious as geopolitical risks and inflation pressures continue to shape the global economic outlook.

June 23, 2025 – Global markets are reacting sharply after a surprise escalation in the Middle East, pushing oil prices higher and rattling investor confidence. Meanwhile, fresh data from Japan hints at a modest recovery in the manufacturing sector.

🇺🇸 US Stock Futures Edge Lower After Strikes on Iran

Stock futures dipped early Monday after the United States launched airstrikes on three Iranian nuclear sites over the weekend. The move, which came sooner than expected, has raised fears of retaliation from Tehran and broader regional instability.

President Donald Trump, who had suggested on Friday he’d wait “two weeks” before making a decision, warned Saturday that “there will be either peace, or there will be tragedy for Iran far greater than we have witnessed over the last eight days.”

What’s at Stake:

Potential Iranian retaliation targeting US assets or personnel

Disruption of oil shipments through the Strait of Hormuz

Heightened volatility across energy and equity markets

🛢️ Oil Prices Surge on Supply Fears

WTI crude oil rose over 2% to $75.90 per barrel, reaching its highest level since January 2025. The market is responding to concerns that Iran may restrict oil exports or block the Strait of Hormuz, a crucial artery for about 20% of global crude oil flows.

Iran’s parliament has reportedly voted to close the Strait, though final approval is pending from the country’s Supreme National Security Council and Supreme Leader.

📉 Market Caution Builds

Major US indexes ended last week little changed, as investors braced for worsening geopolitical tensions and growing economic uncertainty. Risk appetite remains subdued as markets await further developments in the Middle East.

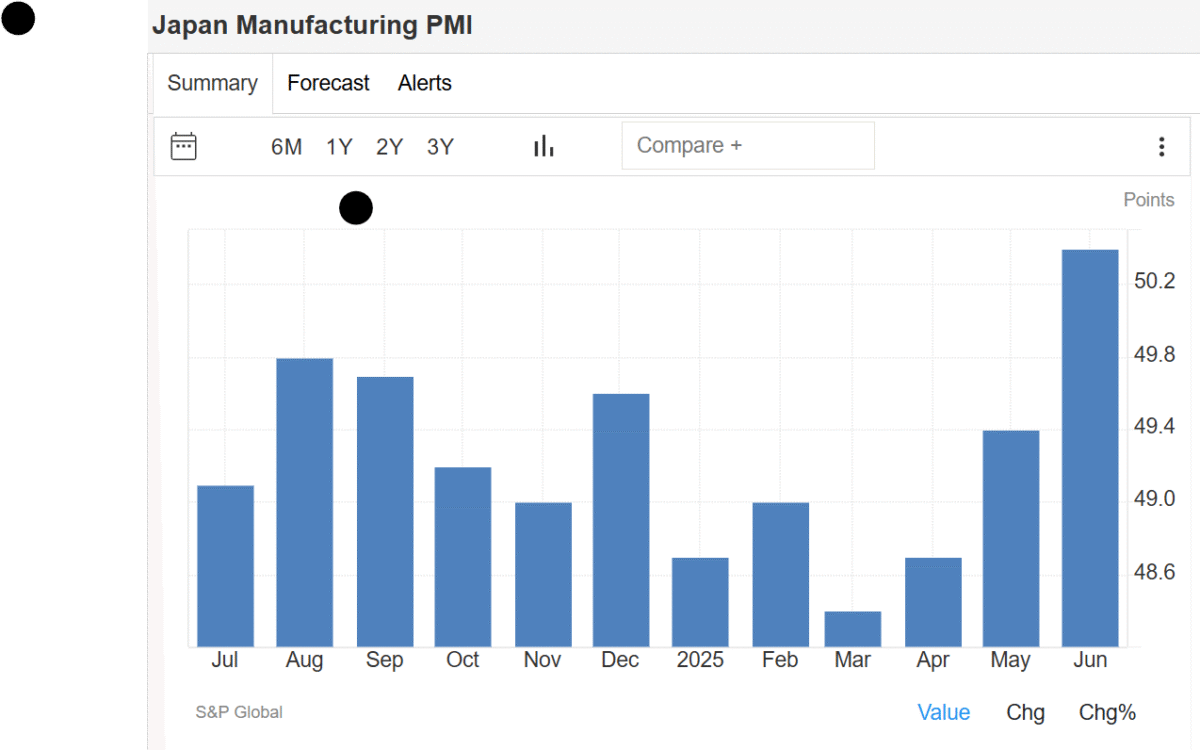

🇯🇵 Japan’s Manufacturing Sector Returns to Growth

On a more positive note, Japan’s Manufacturing PMI from au Jibun Bank rose to 50.4 in June, up from 49.4 in May, marking the first expansion since May 2024. source: S&P Global

Key Highlights:

Output and inventory levels rose

Employment edged higher

Demand remained weak, especially due to new US tariffs

Supplier delivery times lengthened, signaling supply chain pressure

While input cost inflation held near a 14-month low, output prices remained among the softest seen in four years. Business sentiment was largely unchanged and still below the historical average.

📌 Final Takeaway

The Middle East situation is developing rapidly and will likely remain the dominant market driver in the short term. Investors should keep an eye on:

Iran’s next move

Oil market dynamics

Safe-haven assets like gold and the US dollar

Meanwhile, Japan’s modest manufacturing recovery offers a sliver of optimism amid global turbulence.

🇯🇵 Japanese Yen Strengthens as BOJ Eyes Inflation Risks

The Japanese yen gained strength on Friday, trading near ¥145 per U.S. dollar, as Japan’s core inflation surged for the third consecutive month. The latest reading came in at 3.7%, marking the highest level since January 2023 and reinforcing expectations that the Bank of Japan (BOJ) could tighten monetary policy further.

Key Highlights:

BOJ keeps interest rate at 0.5% but signals openness to further hikes.

Governor Kazuo Ueda emphasized a data-driven approach.

Despite Friday’s rebound, the yen is still down ~1% for the week due to safe-haven flows into the U.S. dollar, amid rising geopolitical tensions between Israel and Iran.

📊 Takeaway: A stronger yen may be on the horizon if inflation remains persistent and the BOJ follows through with rate hikes. However, global risk sentiment and U.S. dollar strength are key counterweights.

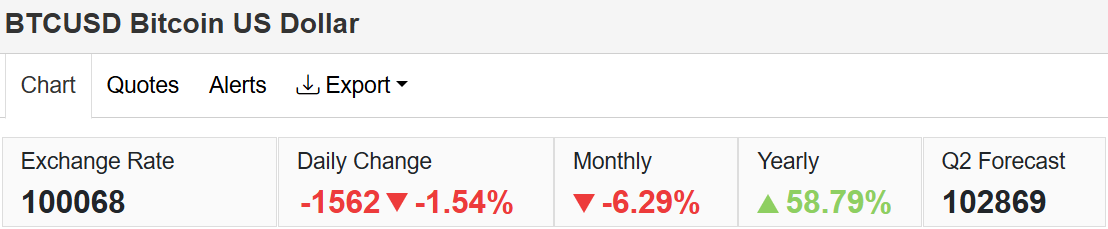

On Sunday, June 22, Bitcoin (BTC/USD) fell to $99,449, marking a 2.15% decline from the previous session. Over the past month, Bitcoin has lost 7.32%, reflecting broader risk-off sentiment across markets.

Bitcoin Performance Overview:

Daily: -2.15%

4-week: -7.32%

12-month: +57.06%

Price Forecasts (via Trading Economics):

End of Q2 2025: $102,869

12-Month Outlook: $100,787

💡 Outlook: Despite short-term dips, long-term fundamentals and macro trends suggest Bitcoin may stabilize or climb moderately in the coming months. However, global tensions and central bank policies could add continued volatility.

🌍 Final Thoughts

Both traditional currencies like the yen and digital assets like Bitcoin are being shaped by a complex macroeconomic environment, featuring persistent inflation, central bank shifts, and geopolitical unrest.

What to Watch:

Next BOJ policy meeting and inflation reports.

U.S. Federal Reserve commentary on rates and inflation.

Developments in the Middle East and their impact on safe-haven assets.

📰 Stay Informed: Subscribe for weekly macro updates and in-depth analysis on currencies, crypto, and global markets.

In a year already fraught with volatility and economic uncertainty, it’s always reassuring to see our thesis confirmed by none other than the legendary Michael Burry. In his latest 13F filing, Burry’s portfolio adjustments echo what many of us have been preparing for: a recessionary reset, an asset repricing, and a rare opportunity to make serious money if you’re positioned right.

In this post, we break down:

Key takeaways from Burry’s 13F

What Buffett and BlackRock’s Larry Fink are signaling

Actionable strategies to optimize your portfolio

How to hedge risk, earn swaps, and profit from market chaos

📌 Key Takeaways from Michael Burry’s 13F Filing (Q1 2025)

Burry has trimmed exposure and taken a sharply defensive stance. Here’s what stands out:

✅ Fewer total holdings – indicating caution

🛡️ Defensive sectors (healthcare, utilities) are up

⚠️ Put options and hedges still in play – suggesting he expects more pain ahead

He’s not alone. Warren Buffett has raised cash, and Larry Fink is leaning heavily on bonds and ESG resilience. Big money is playing defense.

📉 Recession Indicators You Can’t Ignore

1. Inverted Yield Curve

This recession classic has been flashing red for over 12 months — historically a clear precursor to contraction.

2. LEI Index (Leading Economic Index)

Steep and consistent declines in this index are signaling weakening business confidence and slowing economic activity.

3. Consumer Debt Crisis

With rising credit card balances and growing delinquency rates, consumers are stretched thin — a recipe for demand destruction and asset repricing.

💄 Lipstick Effect & Changing Consumer Behavior

When people cut back, they still splurge on small luxuries — a phenomenon known as the lipstick effect. But this signals trouble:

Mid-tier retail is hurting

Premium brands see temporary support

Discretionary spending is collapsing under debt pressure

🧟♂️ Time to Cut the Zombies

Higher rates are suffocating “zombie companies” — those dependent on cheap debt to survive. Their fall will be sharp and painful… but it’s also a generational buying opportunity in real assets and healthy balance sheets.

📊 Sample Recession-Ready Portfolio Allocation

Here’s how to position your portfolio over the next 3–9 months:

Asset Class

Weight

Purpose

💵 Cash / Short-Term Bonds

20%

Dry powder & safety

🛡️ Defensive Equities

15%

Recession resilience (e.g. JNJ, KO, XLU)

💎 High-Quality Value Stocks

10%

Buffett-style buys

🥇 Commodities

15%

Hedge inflation, supply shocks

📉 Inverse ETFs & Puts

10%

Bear market hedge

🌍 Swap Hunter FX Positions

10%

Earn yield & hedge currency risks

📈 EM Equities (Targeted)

5%

High risk/reward bets

⚠️ Speculative / Event-driven

5%

Distressed tech, TLT, etc.

🪙 Gold Miners / Crypto Hedge

5%

Crisis alpha

🧠 Pro tip: Don’t hold inverse ETFs forever. Rotate and hedge tactically.

🔄 Recession Scenario Stress Test

Scenario

Equities

Commodities

Portfolio Impact

Mild Recession

-10%

+5–10%

+2–5% overall

Hard Landing

-25%

-10%

Flat to slightly down

Inflation Spike Returns

+5%

+15%

+7–10% gain

🧩 Bonus: Options Hedge Strategy

Build a recession collar:

✅ Long Puts on SPY/QQQ

✅ Short Calls on KO/JNJ (income)

✅ Long VIX Calls (spike protection)

✅ Conclusion: Don’t Just Survive—Position to Thrive

We’re entering a once-in-a-decade macro reset. Whether you’re following Burry’s lead, watching Buffet’s trims, or managing Swap Hunter FX trades — this is not the time to sit still. Position yourself defensively, keep dry powder ready, and don’t fear the correction — embrace it.

🚀 Ready to Take Action?

Want help building this portfolio, rebalancing your FX swaps, or optimizing your hedges? Let’s talk. Drop a comment, or reach out directly for custom strategy guidance.

🔔 Subscribe for More:

Get weekly macro outlooks, portfolio models, and trading strategies right in your inbox. Sign up now and stay ahead of the herd.

Stay informed with today’s key macroeconomic and market highlights from the U.S., Japan, Germany, and global equity markets.

🇺🇸 U.S. Manufacturing Remains in Contraction

The Philadelphia Fed Manufacturing Index held steady at -4.0 in June 2025, unchanged from May and below market expectations of -1. This marks another month of subdued regional manufacturing activity.

Key Highlights:

New orders stayed positive but weakened.

Shipments improved and turned positive.

Employment fell sharply, reaching its lowest level since May 2020, signaling a drop in factory jobs.

Price pressures eased slightly but remain historically high.

Outlook: Business optimism is waning, with fewer firms expecting growth in the next six months.

👉 Takeaway: Continued weakness in manufacturing could influence the Fed’s policy stance going forward.

🇯🇵 Japan Inflation Eases, Core CPI Surges

Japan’s annual inflation rate fell slightly to 3.5% in May 2025, down from 3.6% in the previous two months. However, core inflation (excluding fresh food and energy) rose to 3.7%, the highest in over two years.

Breakdown:

Declines in prices for clothing, healthcare, and household goods.

Housing, recreation, and communications saw rising costs.

Rice prices skyrocketed over 100% year-over-year, showing limited impact from government price controls.

👉 Takeaway: Inflation remains a concern ahead of Japan’s summer elections, adding complexity to BoJ policy decisions.

🇩🇪 German Producer Prices Drop Sharply

Germany’s Producer Price Index (PPI) fell 1.2% year-over-year in May 2025, marking the third straight month of decline and the sharpest drop since September 2024.

Details:

Energy prices fell sharply:

Electricity: -8.1%

Natural gas: -7.1%

Heating oil: -10.2%

Excluding energy, producer prices rose 1.3% YoY.

Monthly PPI dropped 0.2%, better than the expected 0.3% decline.

👉 Takeaway: Cooling input prices support the ECB’s disinflation narrative but won’t remove all pressure from sticky core inflation.

📊 U.S. Markets Set for a Lower Open

After Wednesday’s Juneteenth holiday, U.S. stock futures point to a slightly lower open as investors react to:

Ongoing geopolitical tensions in the Middle East.

President Trump’s delayed decision on Iran, while strikes from Israel continue.

Oil prices retreat, weighing on energy stocks.

CarMax expected to open 10%+ higher after strong earnings.

Triple Witching Day could increase market volatility.

👉 Takeaway: Risk appetite remains fragile. Expect choppy trading as geopolitical uncertainty and technical factors weigh on sentiment.

📌 Final Thoughts

Economic data continues to paint a mixed global picture—slowing growth, sticky inflation, and rising geopolitical risks. Investors should brace for near-term volatility and monitor central bank signals closely.

Established in 2005 a Trusted Broker with 20 years in the Industry

Trade over 20,000 instruments including Forex, Metals, Shares, Indices, Commodities & Cryptocurrencies.

Security of funds $1,000,000 Excess Loss Insurance policy with Lloyd’s of London

regulated by ASIC, AUSTRAC, BAFIN, CIMA, ESCA, CySEC, FSC, FMA, MAS, TFG and VFSC.

25+ Offices Located within the Financial Centres of the World