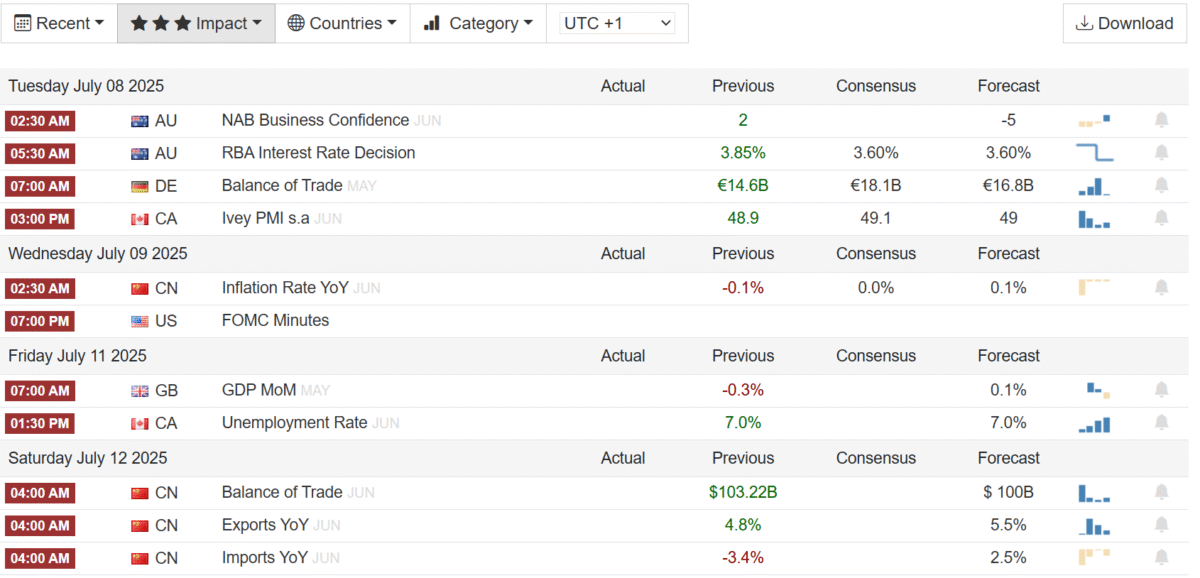

Trade Tensions Return: The July 9th deadline marks the end of the US tariff pause. Only partial deals (UK, Vietnam, China framework) are in place. Markets are bracing for possible escalations and their impact on global trade flows.

Fed Watch: Investors await the FOMC minutes and several Fed speeches to gauge the outlook for interest rates. Chair Powell maintains a cautious tone, but markets want more clues on the path for policy in H2.

Central Bank Decisions: Policy meetings in Australia, South Korea, Malaysia, and New Zealand could signal regional divergence amid slowing global growth and easing inflation.

🇺🇸 United States

Tariff Deadline: High stakes around the July 9th expiration of tariff relief. Key sectors may face higher import costs unless further agreements are reached.

Fed & Data:

FOMC minutes and Fed speeches in focus.

Data includes: Weekly jobless claims, consumer credit, NFIB Small Business Index, and budget statement.

Earnings Season Kickoff:

Watch Delta Air Lines and Conagra Brands earnings on Thursday for early corporate sentiment.

🇨🇦 Canada

June Jobs Report and Ivey PMI will shape expectations around Bank of Canada’s next move.

🇲🇽 Mexico & 🇧🇷 Brazil

Mexico: June inflation report will guide Banxico’s next rate decision.

Brazil: Updates on inflation, retail sales, and business confidence are due.

🇪🇺 Europe

Germany: Expected second monthly industrial production decline, plus trade, wholesale prices, and final inflation data.

Eurozone: First dip in retail sales in 5 months.

UK: Key data on monthly GDP, industrial output, trade balance, and Halifax house prices.

Italy & France: Final inflation and industrial figures.

Others: Switzerland (consumer confidence), Turkey (IP), Russia (inflation).

🌏 Asia-Pacific

China:

CPI likely flat; PPI deflation to ease (still -3.2% y/y).

Japan:

Full slate of data: wages, current account, machine orders, producer prices.

U.S. Nonfarm Payrolls Rise 147K in June, Topping Expectations

The U.S. economy added 147,000 jobs in June 2025, according to the Bureau of Labor Statistics, surpassing forecasts of 110,000 and marking a slight uptick from an upwardly revised 144,000 in May. The latest reading aligns with the 12-month average of 146,000, continuing to demonstrate labor market resilience despite economic headwinds.

Government jobs made up nearly half the gains, adding 73,000 positions, primarily in state education (+40K) and local education (+23K). Federal government employment, however, declined by 7,000, continuing a downtrend since its January peak.

Healthcare remained a key driver, adding 39,000 jobs, with hospitals (+16K) and nursing and residential care facilities (+14K) leading the way. Social assistance roles also grew by 19,000.

⚠️ Analysts caution that a hiring slowdown could emerge as uncertainty surrounding tariffs, trade, and immigration policies persists.

ISM Services PMI Rebounds to 50.8

The ISM Services PMI climbed to 50.8 in June, up from 49.9 in May, exceeding expectations of 50.5. This signals a return to modest growth in the services sector after a brief contraction.

Key highlights:

Business activity rose to 54.2 (vs 50.0)

New orders rebounded to 51.3 (vs 46.4)

Inventories and export orders also improved

Price pressures eased slightly to 67.5 from 68.7

However, concerns about tariffs and slowing supplier delivery performance (50.3 vs 52.5) remain prevalent. Middle East tensions were noted for the first time, though no direct supply disruptions were reported.

U.S. Trade Deficit Widens Sharply

The U.S. trade deficit widened to $71.5 billion in May, up from $60.3 billion in April, as exports dropped 4% to $279 billion, led by declines in nonmonetary gold, natural gas, and finished metal shapes. Imports dipped just 0.1% to $350.5 billion.

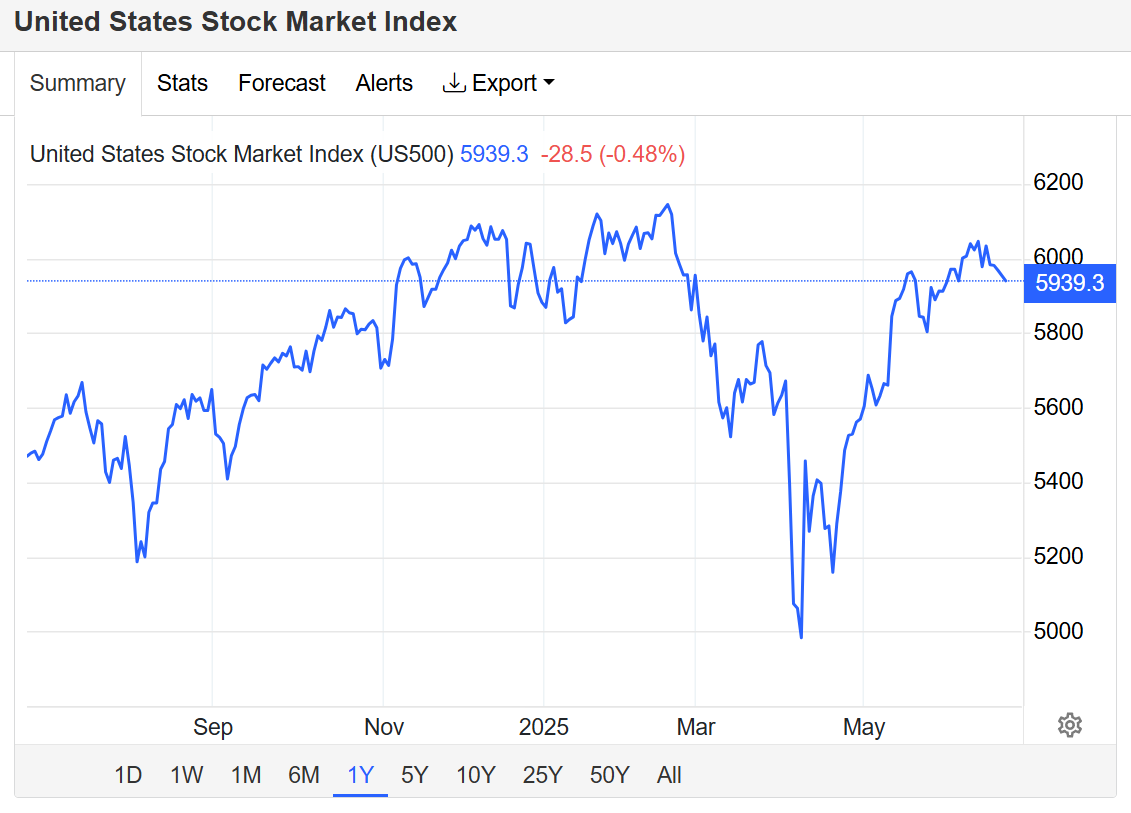

All three major U.S. indices climbed over 0.8% on Thursday, with the S&P 500 and Nasdaq 100 closing at record highs. The strong June payroll report and an unexpected drop in the unemployment rate to 4.1% fueled investor confidence.

Big movers:

Nvidia: +1.3%

Synopsys: +4.2% on lifted U.S. export restrictions to China

Cadence Design & Synopsys: ~+5% on AI strength

Datadog: +10% on S&P 500 inclusion

Optimism also stemmed from progress in the U.S.-Vietnam trade deal and the House nearing final approval of President Trump’s $3.4 trillion tax-and-spending bill.

Key Takeaways

Labor market continues to show strength but faces downside risks.

Services sector rebounds, though growth remains modest.

Trade imbalance widens on export slump.

Stock market surges on tech gains and policy optimism.

Conclusion

The June 2025 economic indicators paint a mixed yet cautiously optimistic picture. While the labor market and services sector show resilience, trade imbalances and policy uncertainty loom large. Investors appear encouraged by tech sector momentum and fiscal stimulus prospects, but volatility could reemerge as global tensions and trade debates evolve.

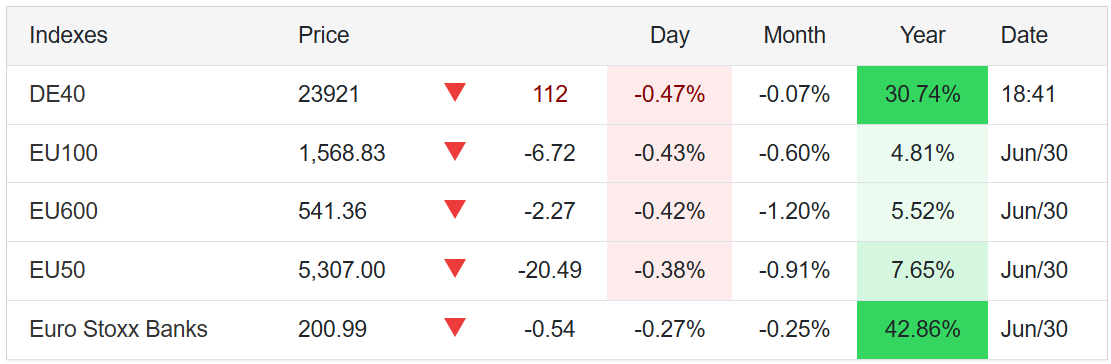

📊 Germany Stock Market Index (DE40) Falls Amid Economic Uncertainty

The Germany Stock Market Index (DE40)—which tracks the performance of 40 top German blue-chip stocks—closed down 0.5% at 23,910 on Monday, breaking a two-day winning streak. The decline comes amid mixed domestic economic data and renewed trade concerns.

🇩🇪 Key Economic Indicators in Germany

✅ Inflation Cools in June

German inflation surprised markets by dropping to 2.0% year-on-year in June, down from 2.1% in May and below the 2.2% forecast. This signals easing price pressure, potentially giving the European Central Bank (ECB) more flexibility on interest rates.

❌ Retail Sales Point to Weak Consumer Demand

Germany’s retail sales fell 1.6% in May, following a 0.6% drop in April. This back-to-back decline underlines sluggish domestic consumption, a key factor limiting broader economic recovery in Europe’s largest economy.

🌐 Trade Tensions Add Market Pressure

Global trade uncertainty continues to weigh on the German stock market. U.S. President Trump confirmed that trade negotiations are ongoing but won’t extend the current 90-day tariff pause beyond July 9. This raises risks for Germany’s export-heavy economy, especially sectors like automotive and chemicals.

🔻 Biggest DAX Losers: Symrise and Bayer

Symrise AG led the market declines with a sharp 7% drop, likely due to sector sentiment or earnings-related concerns.

Bayer AG tumbled 5.4% after the U.S. Supreme Court requested the government’s opinion on Monsanto weedkiller litigation, reigniting legal uncertainty for the pharma and agrochemical giant.

📆 DE40 Monthly Performance

Despite occasional gains, the DAX (DE40) ended June with a modest 0.4% loss, reflecting ongoing macroeconomic headwinds and market caution.

📌 What to Watch Next

July 9 Trade Deadline: Markets will closely monitor whether new tariffs are imposed.

Upcoming ECB Decisions: Slower inflation may influence monetary policy.

📈 US Stocks Surge as Fed Cut Hopes and Trade Truce Drive Gains

Published: June 30, 2025 Category: Markets & Economy

US equities rallied on Monday, extending last week’s gains as easing trade tensions and growing expectations of interest rate cuts by the Federal Reserve pushed major indexes to record highs.

🔼 Major Indexes Reach New Highs

S&P 500 and Nasdaq 100: Up 0.5% each

Dow Jones Industrial Average: Gained over 200 points

📰 Market Drivers

1. 🇺🇸 US-China Trade Agreement

The US and China announced a formal agreement to prevent new tariffs, with President Trump showing flexibility on the July 9 deadline for reintroducing reciprocal tariffs. This marks a major de-escalation from past tensions, when tariffs reached up to 145%.

2. 🏦 Fed Rate Cut Expectations Rise

Investor confidence is rising as soft inflation data and global uncertainties increase the likelihood of multiple Fed rate cuts in 2025.

3. 💻 Tech Sector Strengthens

Canada scrapped its digital services tax, boosting US tech stocks and reopening trade talks.

Meta and Alphabet shares rose 1%.

Juniper Networks soared 9% after the DoJ approved its HP acquisition, settling a legal dispute.

💶 Eurozone: Euro Hits $1.17 as German Inflation Falls

The euro rose to its highest level since September 2021, trading just above $1.17, bolstered by:

Weaker US dollar from dovish Fed sentiment

Fiscal concerns in the US

Cooling inflation in Germany

🇩🇪 Germany Inflation Back to Target

According to the Federal Statistical Office:

CPI fell to 2.0% in June, down from 2.1%, beating forecasts

Core inflation eased to 2.7%, a 3-month low

Food inflation slowed to 2.0%, energy prices dropped -3.5%

Monthly CPI was flat, following a 0.1% rise in May

🏦 ECB Policy Outlook

While inflation edged up slightly in France, Italy, and Spain, the ECB maintains a cautious approach. Vice President Luis de Guindos reaffirmed that the current policy is appropriate, but warned of the need for flexibility amid economic uncertainty.

Markets continue to price the ECB’s terminal rate around 1.75%–1.80%.

📊 Key Takeaways

✅ US markets are responding positively to reduced geopolitical risk and a potential easing cycle from the Fed.

✅ Eurozone inflation data provides mixed signals but supports a stable ECB outlook.

✅ Tech stocks may continue to benefit from regulatory relief and favorable trade shifts.

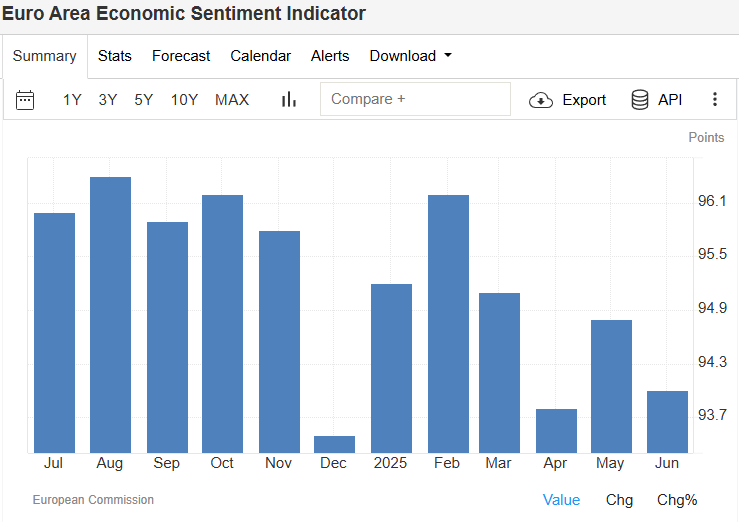

Euro Area Economic Sentiment Indicator Falls to 94 in June 2025

The Economic Sentiment Indicator (ESI) for the Euro Area dropped to 94 in June 2025, down from 94.8 in May and well below market expectations of 95.1, according to the latest data from the European Commission.

📉 Key Drivers of the Decline

The drop in sentiment was largely driven by the industrial sector, where confidence slipped to -12 from -10.4 in the previous month. The decline reflects:

Lower order book assessments

Higher stocks of finished products

Weaker production expectations

Additional declines were observed in:

Retail confidence: -7.5 (vs -7.2 in May)

Consumer confidence: -15.3 (vs -15.1)

📈 Sectors Showing Improvement

Despite the overall downturn, two sectors posted gains:

Services: Confidence improved to 2.9 (from 1.8)

Construction: Rebounded slightly to -2.8 (from -3.5)

🌍 Country-Level Highlights

Biggest Declines:

France: 89.6 (down from 93)

Spain: 102 (down from 103.4)

Germany: 90.7 (down from 91.5)

Stable or Improving:

Poland: 101.4 (up from 100.4)

Italy: 98.9 (vs 98.7)

Netherlands: 97.1 (vs 96.9)

🔎 What It Means for the Eurozone

The data suggest ongoing economic weakness across the Eurozone, particularly in manufacturing and retail sectors. While services and construction offer some support, the overall picture points to fragile business and consumer confidence as the region navigates 2025.

This divergence between countries—particularly the downturn in France and Germany—highlights uneven recovery dynamics within the EU bloc. source: European Commission

Stay tuned for more updates on EU economic indicators and what they mean for markets and policy.

WTI crude oil, gold prices, and the US dollar index all moved significantly on Thursday as geopolitical developments, Fed policy signals, and economic data shaped market sentiment.

Crude Oil Prices Rise Ahead of US–Iran Talks and OPEC+ Meeting

WTI crude oil futures climbed above $65 per barrel on Thursday, building on recent gains and recovering from earlier losses in the week. The rally comes as investors await high-stakes talks between the US and Iran scheduled for next week. These discussions aim to reduce tensions in the Middle East and limit Tehran’s nuclear ambitions.

The move follows President Trump’s reaffirmation of the maximum pressure campaign, including restrictions on Iranian oil exports. However, he also hinted at possible enforcement leniency to support Iran’s reconstruction, suggesting China may continue importing Iranian crude.

In a sign of strong demand, US crude inventories dropped by 5.8 million barrels, reaching an 11-year seasonal low. Cushing stockpiles also fell to the lowest since February.

Markets are now turning their focus to the upcoming OPEC+ meeting on July 6, where the group will set its production policy for August. Russia may support a supply increase if conditions warrant it.

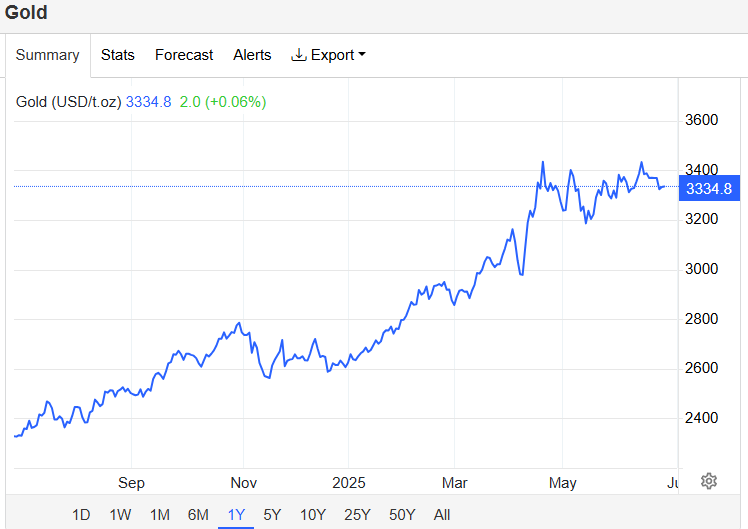

Gold Prices Edge Higher on Weaker Dollar, Geopolitical Relief

Gold prices rose toward $3,340 per ounce, extending gains from the previous session. The weaker US dollar and falling Treasury yields provided support, while easing geopolitical tensions added a further boost.

Next week’s US–Iran talks have sparked cautious optimism in markets. While the ceasefire between Iran and Israel is holding, concerns about its durability remain.

Meanwhile, Fed Chair Jerome Powell, in his second day of testimony, maintained a balanced stance—acknowledging inflation risks from tariffs but holding off on immediate rate cuts. Nonetheless, weak consumer confidence in June raised fresh concerns about the labor market and trade uncertainty, potentially strengthening the case for future easing.

Markets are now closely watching key data, including Thursday’s final Q1 GDP reading and initial jobless claims, followed by PCE price data on Friday.

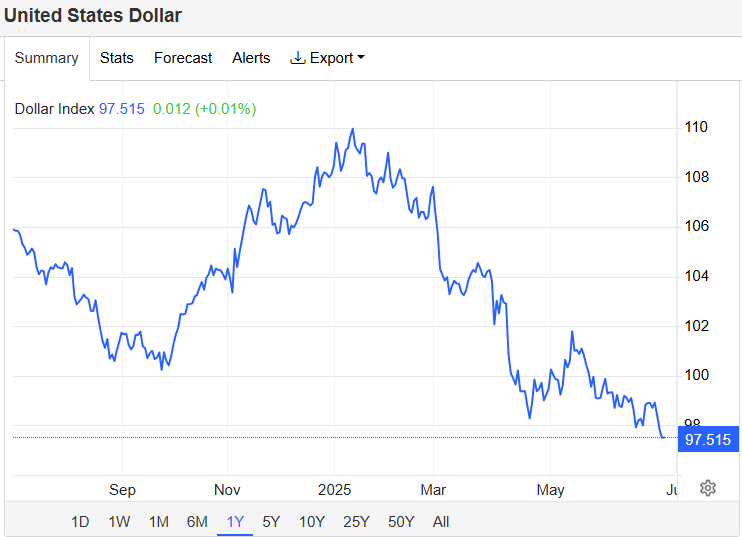

US Dollar Slides to Three-Year Low Amid Rate Cut Expectations

The US dollar index fell to around 97.5, marking its lowest level in over three years. The decline reflects a mix of easing geopolitical tensions, growing fiscal worries, and expectations of Federal Reserve rate cuts.

With the ceasefire between Iran and Israel seemingly stable and US–Iran negotiations on the horizon, risk sentiment improved. On the policy front, Chair Powell reiterated a cautious stance, stating that while tariffs may drive inflation, the Fed would likely continue easing absent those pressures.

Traders are now pricing in over 60 basis points of rate cuts by year-end, with the next move anticipated in September. Attention is also turning to US trade negotiations ahead of President Trump’s July 9 deadline, and efforts in Congress to finalize a tax and spending package around the same period.

Looking Ahead

Markets are poised for more volatility as geopolitical, economic, and policy developments continue to unfold. Investors should watch closely for:

US–Iran nuclear talks next week

July 6 OPEC+ meeting outcomes

Upcoming US economic data (GDP, jobless claims, PCE)

Fed policy signals amid global trade uncertainty

Stay tuned for further updates as these stories evolve.

Fill out the registration form below to receive a FREE consultation from Swap Hunter

Open your Trading Account with MEX Atlantic, part of the MultiBank Group

🏠 U.S. New Home Sales Plunge in May 2025 as Buyers Retreat Amid High Mortgage Rates

New single-family home sales in the U.S. fell sharply in May 2025, dropping 13.7% month-over-month to a seasonally adjusted annualized rate of 623,000 units, according to the U.S. Census Bureau. This marks the biggest decline since June 2022, far below market expectations of around 700,000 units.

📉 Housing Market Breakdown:

South: -21% to 349,000 units

West: -5.4% to 159,000 units

Midwest: -7.1% to 78,000 units

Median home price: $507,000 (+1.4%)

Supply: 9.8 months at current sales pace

High mortgage rates and economic uncertainty are causing many potential buyers to delay purchases, signaling a cooling housing market despite rising prices.

📊 Stock Market Update: Tech Leads, Real Estate Lags

The S&P 500 rose 0.2% on Wednesday, while the Nasdaq 100 gained 0.4%, inching closer to a new all-time high. The Dow Jones remained near flatline levels.

Top Performers:

Nvidia: +1.3%

Apple: +1.2%

Microsoft: +0.6%

Amazon: +1.1%

Meta: +0.2%

Underperformers:

Real Estate sector (reflecting weak housing data)

FedEx: -5% after disappointing profit forecast

Investor sentiment was buoyed by Fed Chair Jerome Powell’s dovish testimony before Congress, which reinforced expectations of at least two interest rate cuts by the end of 2025. In addition, a ceasefire between Iran and Israel helped calm global markets.

💵 Dollar Index Holds as Fed Signals Policy Flexibility

The U.S. Dollar Index (DXY) held steady at 98 on Wednesday, pausing its recent slide to multi-year lows.

Key Drivers:

Powell’s remarks: Economic uncertainty justifies patience on interest rates

Disinflation outlook: Maintained as long as no new tariffs are introduced (watch for July 9 deadline)

Energy prices: Falling due to stability in the Strait of Hormuz, boosting bets on slowing inflation

Meanwhile, other major economies are also leaning toward monetary easing, helping to stabilize the greenback despite rate cut expectations in the U.S.

📌 Final Thoughts: What to Watch Next

Will housing weakness extend into summer?

Can tech continue to lead the market higher?

July 9 tariff decision will be critical for inflation and Fed policy

Watch for inflation and jobs data to confirm (or challenge) rate cut bets

📬 Stay tuned for more market insights and economic updates. 📢 Don’t forget to share this post and leave a comment below with your thoughts on where the market is headed next!

European Stocks Climb as Ceasefire Holds, Fed Dovish Tone Lifts Sentiment

Markets held onto their upward momentum Wednesday, with the STOXX 50 and STOXX 600 indices both rising 0.3%, extending gains of over 1% from the previous session. Investors were buoyed by easing geopolitical tensions and growing hopes for a Federal Reserve rate cut later this year.

🌍 Geopolitical Calm Brings Relief

The recent ceasefire between Israel and Iran appears to be holding, providing a much-needed breather for global markets. The truce—brokered by the United States—has helped temper fears of a broader conflict in the Middle East, a key concern for global investors in recent weeks.

📉 Fed Signals Potential Rate Cuts

Further optimism was driven by Federal Reserve Chair Jerome Powell, who gave testimony before the U.S. Congress on Tuesday. His remarks were widely interpreted as dovish, increasing expectations that the Fed could cut interest rates later this year, providing additional support to financial markets.

🔍 Focus Shifts to NATO Summit

Investors are now watching the NATO summit in the Netherlands, where discussions around defense spending and geopolitical stability are taking center stage. Any shifts in policy or alliances could have broader market implications.

Winners on the European Stock Front

Several major companies posted strong gains amid the upbeat mood:

Ferrari (RACE): +3.6%

Stellantis (STLA): +3.7%

ASML Holding (ASML): +2.3%

Philips (PHG): +2.0%

Rheinmetall (RHM): +1.5%

These moves reflect renewed investor confidence across a range of sectors, from luxury autos to defense and technology.

Crude Oil Bounces Back After Heavy Selloff

WTI crude oil prices rebounded above $65 per barrel on Wednesday, recovering some ground after a 13% plunge over the prior two sessions—the steepest two-day fall since 2022.

🔥 What’s Driving Oil?

The ceasefire in the Middle East is reducing supply disruption fears.

President Trump signaled support for China—Iran’s top buyer—to continue importing Iranian oil, potentially reshaping the U.S. sanctions landscape.

Despite this, a preliminary U.S. intelligence report warned that American strikes on Iranian nuclear facilities only delayed the program by a few months, keeping geopolitical risk on the table.

📉 Supply Tightens

Fresh industry data revealed a 4.28 million barrel drop in U.S. crude inventories last week, smashing forecasts for just a 0.6 million barrel draw. This marks the fourth consecutive weekly decline and signals tightening supply conditions.

🧠 Final Thoughts

Markets are finding their footing amid complex global dynamics. While the ceasefire and dovish Fed tone provide near-term relief, investors remain cautious as geopolitical risks and inflation pressures continue to shape the global economic outlook.

🇯🇵 Japanese Yen Strengthens as BOJ Eyes Inflation Risks

The Japanese yen gained strength on Friday, trading near ¥145 per U.S. dollar, as Japan’s core inflation surged for the third consecutive month. The latest reading came in at 3.7%, marking the highest level since January 2023 and reinforcing expectations that the Bank of Japan (BOJ) could tighten monetary policy further.

Key Highlights:

BOJ keeps interest rate at 0.5% but signals openness to further hikes.

Governor Kazuo Ueda emphasized a data-driven approach.

Despite Friday’s rebound, the yen is still down ~1% for the week due to safe-haven flows into the U.S. dollar, amid rising geopolitical tensions between Israel and Iran.

📊 Takeaway: A stronger yen may be on the horizon if inflation remains persistent and the BOJ follows through with rate hikes. However, global risk sentiment and U.S. dollar strength are key counterweights.

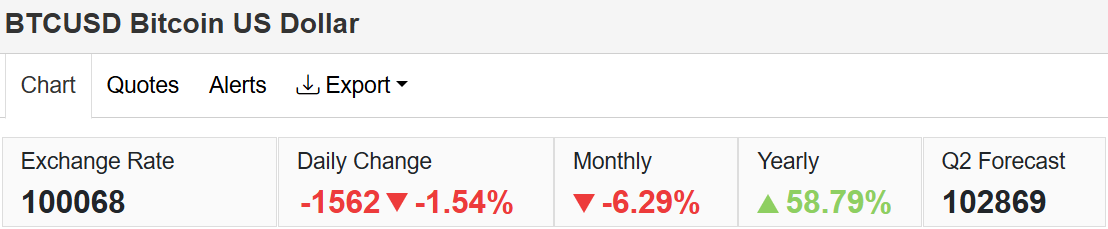

On Sunday, June 22, Bitcoin (BTC/USD) fell to $99,449, marking a 2.15% decline from the previous session. Over the past month, Bitcoin has lost 7.32%, reflecting broader risk-off sentiment across markets.

Bitcoin Performance Overview:

Daily: -2.15%

4-week: -7.32%

12-month: +57.06%

Price Forecasts (via Trading Economics):

End of Q2 2025: $102,869

12-Month Outlook: $100,787

💡 Outlook: Despite short-term dips, long-term fundamentals and macro trends suggest Bitcoin may stabilize or climb moderately in the coming months. However, global tensions and central bank policies could add continued volatility.

🌍 Final Thoughts

Both traditional currencies like the yen and digital assets like Bitcoin are being shaped by a complex macroeconomic environment, featuring persistent inflation, central bank shifts, and geopolitical unrest.

What to Watch:

Next BOJ policy meeting and inflation reports.

U.S. Federal Reserve commentary on rates and inflation.

Developments in the Middle East and their impact on safe-haven assets.

📰 Stay Informed: Subscribe for weekly macro updates and in-depth analysis on currencies, crypto, and global markets.

In a year already fraught with volatility and economic uncertainty, it’s always reassuring to see our thesis confirmed by none other than the legendary Michael Burry. In his latest 13F filing, Burry’s portfolio adjustments echo what many of us have been preparing for: a recessionary reset, an asset repricing, and a rare opportunity to make serious money if you’re positioned right.

In this post, we break down:

Key takeaways from Burry’s 13F

What Buffett and BlackRock’s Larry Fink are signaling

Actionable strategies to optimize your portfolio

How to hedge risk, earn swaps, and profit from market chaos

📌 Key Takeaways from Michael Burry’s 13F Filing (Q1 2025)

Burry has trimmed exposure and taken a sharply defensive stance. Here’s what stands out:

✅ Fewer total holdings – indicating caution

🛡️ Defensive sectors (healthcare, utilities) are up

⚠️ Put options and hedges still in play – suggesting he expects more pain ahead

He’s not alone. Warren Buffett has raised cash, and Larry Fink is leaning heavily on bonds and ESG resilience. Big money is playing defense.

📉 Recession Indicators You Can’t Ignore

1. Inverted Yield Curve

This recession classic has been flashing red for over 12 months — historically a clear precursor to contraction.

2. LEI Index (Leading Economic Index)

Steep and consistent declines in this index are signaling weakening business confidence and slowing economic activity.

3. Consumer Debt Crisis

With rising credit card balances and growing delinquency rates, consumers are stretched thin — a recipe for demand destruction and asset repricing.

💄 Lipstick Effect & Changing Consumer Behavior

When people cut back, they still splurge on small luxuries — a phenomenon known as the lipstick effect. But this signals trouble:

Mid-tier retail is hurting

Premium brands see temporary support

Discretionary spending is collapsing under debt pressure

🧟♂️ Time to Cut the Zombies

Higher rates are suffocating “zombie companies” — those dependent on cheap debt to survive. Their fall will be sharp and painful… but it’s also a generational buying opportunity in real assets and healthy balance sheets.

📊 Sample Recession-Ready Portfolio Allocation

Here’s how to position your portfolio over the next 3–9 months:

Asset Class

Weight

Purpose

💵 Cash / Short-Term Bonds

20%

Dry powder & safety

🛡️ Defensive Equities

15%

Recession resilience (e.g. JNJ, KO, XLU)

💎 High-Quality Value Stocks

10%

Buffett-style buys

🥇 Commodities

15%

Hedge inflation, supply shocks

📉 Inverse ETFs & Puts

10%

Bear market hedge

🌍 Swap Hunter FX Positions

10%

Earn yield & hedge currency risks

📈 EM Equities (Targeted)

5%

High risk/reward bets

⚠️ Speculative / Event-driven

5%

Distressed tech, TLT, etc.

🪙 Gold Miners / Crypto Hedge

5%

Crisis alpha

🧠 Pro tip: Don’t hold inverse ETFs forever. Rotate and hedge tactically.

🔄 Recession Scenario Stress Test

Scenario

Equities

Commodities

Portfolio Impact

Mild Recession

-10%

+5–10%

+2–5% overall

Hard Landing

-25%

-10%

Flat to slightly down

Inflation Spike Returns

+5%

+15%

+7–10% gain

🧩 Bonus: Options Hedge Strategy

Build a recession collar:

✅ Long Puts on SPY/QQQ

✅ Short Calls on KO/JNJ (income)

✅ Long VIX Calls (spike protection)

✅ Conclusion: Don’t Just Survive—Position to Thrive

We’re entering a once-in-a-decade macro reset. Whether you’re following Burry’s lead, watching Buffet’s trims, or managing Swap Hunter FX trades — this is not the time to sit still. Position yourself defensively, keep dry powder ready, and don’t fear the correction — embrace it.

🚀 Ready to Take Action?

Want help building this portfolio, rebalancing your FX swaps, or optimizing your hedges? Let’s talk. Drop a comment, or reach out directly for custom strategy guidance.

🔔 Subscribe for More:

Get weekly macro outlooks, portfolio models, and trading strategies right in your inbox. Sign up now and stay ahead of the herd.